EPR — The Policy Engine Behind Pyrolysis Growth

What Is Extended Producer Responsibility?

Extended Producer Responsibility (EPR) is a policy approach that shifts the cost and responsibility for managing end-of-life products from municipalities and taxpayers to the producers who place those products on the market — manufacturers, importers, and brand owners.

Under EPR, producers must fund the collection, sorting, recycling, and environmentally sound disposal of their products once consumers discard them. This creates powerful financial incentives to:

Fund Recycling Infrastructure

Producer fees finance collection, sorting, and processing — creating the economic foundation for advanced recycling plants.

Design for Recyclability

Fee modulation charges higher fees for hard-to-recycle packaging, incentivising simpler, recyclable designs.

Create Demand for Recycled Content

Recycled content mandates and plastic taxes make recycled materials economically competitive with virgin alternatives.

EPR for Plastics — Global Landscape

Plastic EPR has expanded rapidly worldwide. Over 60 countries now have some form of producer responsibility for plastic packaging, with the EU, India, and the UK leading with the most comprehensive frameworks.

| Region | Regulation | Key Targets | Status |

|---|---|---|---|

| 🇪🇺 EU (27 states) | Packaging & Packaging Waste Regulation (PPWR) | Recycled content mandates + recycling rate targets | In Force (Aug 2026) |

| 🇮🇳 India | Plastic Waste Management Rules (PWM) | 60-80% recycling obligation by 2027-28 | Active |

| 🇬🇧 United Kingdom | Packaging EPR (pEPR) + Plastic Packaging Tax | £217.85/t tax on <30% recycled content | Active |

| 🇺🇸 United States | State-level EPR (CA, CO, OR, ME, MN, IL, CT) | Producer-funded recycling programs | Rolling Out |

| 🇨🇦 Canada | Provincial EPR programs (BC, ON, QC, AB) | Full producer responsibility for packaging | Active |

EU Packaging & Packaging Waste Regulation (PPWR)

The PPWR is the most impactful EPR regulation for pyrolysis globally. Entering into force in August 2026, it mandates recycled content in plastic packaging across all 27 EU member states — creating massive demand for chemical recycling output that only pyrolysis can supply at scale.

India — Aggressive EPR Targets for Plastics

India's Plastic Waste Management (PWM) Rules impose some of the world's most ambitious EPR obligations. Producers, importers, and brand owners must meet escalating recycling targets from 60% to 80% of their plastic packaging output by 2027-28. EPR certificates are tradeable, creating a market mechanism that rewards recycling capacity.

With India generating 3.5+ million tonnes of plastic waste annually and mechanical recycling capacity insufficient to meet targets, pyrolysis-based chemical recycling is emerging as the critical gap-filler — particularly for multilayer and contaminated plastics that mechanical recyclers reject.

Automated pyrolysis plant meeting EPR capacity demands

EPR for Tires

Tire EPR is well-established globally and has been a proven driver of tire pyrolysis investment. Unlike plastic EPR which is still evolving, tire EPR has decades of operational history in Europe.

🇪🇺 EU — 21+ Countries

Producer Responsibility Organisations (PROs) manage end-of-life tires across 21+ EU countries. France (Aliapur), Germany, Spain, Italy, and others have mature tire EPR systems. Pyrolysis is an approved processing method in most frameworks.

🇮🇳 India — 100% Target

India mandates 100% EPR obligations for tire producers. The Extended Producer Responsibility framework covers all tire manufacturers and importers, driving investment in tire pyrolysis infrastructure.

🇺🇸 US — Connecticut (2026)

Connecticut enacted the first comprehensive US tire EPR law, effective March 2026. Producers must fund collection and recycling of end-of-life tires — a model likely to be adopted by other states.

🇨🇦 Canada — Provincial Programs

Canadian provinces operate mature tire stewardship programs. British Columbia, Ontario, Quebec, and Alberta have established collection and recycling infrastructure funded by eco-fees on new tires.

Tire Pyrolysis Under EPR

Tire EPR provides a guaranteed feedstock supply for pyrolysis operators. With mandatory collection rates above 90% in most EU countries and India targeting 100%, end-of-life tires are one of the most reliable waste feedstocks available. APChemi designs tire pyrolysis plants that produce pyrolysis oil, recovered carbon black (rCB), and steel — maximising value extraction from EPR-collected tires.

Planning a pyrolysis project to capture EPR-driven demand? APChemi designs ISCC-certifiable plants that produce circular feedstock meeting regulatory requirements. Discuss your project.

How EPR Drives Pyrolysis Demand

EPR creates demand for pyrolysis through three interconnected mechanisms that together form a powerful growth engine for the industry.

Feedstock Supply (Push)

Mandatory collection and sorting targets under EPR dramatically increase the volume of waste plastic and tires entering the recycling system. Much of this material — multilayer packaging, contaminated plastics, mixed polymers — cannot be mechanically recycled and needs chemical recycling via pyrolysis. EPR ensures a steady, growing supply of feedstock.

Recycled Content Mandates (Pull) Biggest Driver

Regulations like the EU PPWR mandate minimum recycled content in new plastic products. Mechanical recycling cannot produce food-grade recycled content for most plastics, and its output degrades with each cycle. Pyrolysis-based chemical recycling is the only scalable pathway to produce virgin-quality recycled plastics — making it essential for regulatory compliance.

Financial Incentives (Economics)

EPR fee modulation, plastic packaging taxes, and tradeable recycling certificates create direct financial incentives for chemical recycling. The UK Plastic Packaging Tax of £217.85/tonne on packaging with <30% recycled content, for example, makes chemically recycled feedstock highly cost-competitive versus virgin plastics.

Recycled Content Mandates

Recycled content mandates are the most direct mechanism linking EPR to pyrolysis demand. They require producers to include minimum percentages of recycled material in new products — and only chemical recycling can meet these targets for food-contact and high-performance applications.

| Regulation | Material | 2030 Target | 2040 Target |

|---|---|---|---|

| EU PPWR | Contact-sensitive PET packaging | 30% | 50% |

| Other contact-sensitive plastics | 10% | 25% | |

| Non-contact-sensitive plastics | 35% | 65% | |

| India PWM Rules | Rigid & flexible packaging | 60-80% | — |

| UK Plastic Packaging Tax | All plastic packaging | 30% minimum | Under review |

Why Mechanical Recycling Alone Cannot Meet These Targets

✕ Mechanical Recycling Limits

- ● Cannot produce food-contact-grade recyclate for PE/PP

- ● Quality degrades with each cycle (2-3 max)

- ● Rejects multilayer and contaminated plastics

- ● Limited to clean, sorted single-polymer streams

✓ Chemical Recycling (Pyrolysis)

- ● Produces virgin-quality, food-contact-grade output

- ● Infinitely recyclable — no quality degradation

- ● Handles mixed, multilayer, and contaminated waste

- ● ISCC mass balance enables certified recycled content

Market Opportunity

EPR regulations are creating a massive market opportunity for pyrolysis operators. The combination of mandatory collection, recycled content mandates, and financial incentives is driving billions in investment.

EPR-Driven Market Opportunity for Pyrolysis

Why the Market Is Growing Fast

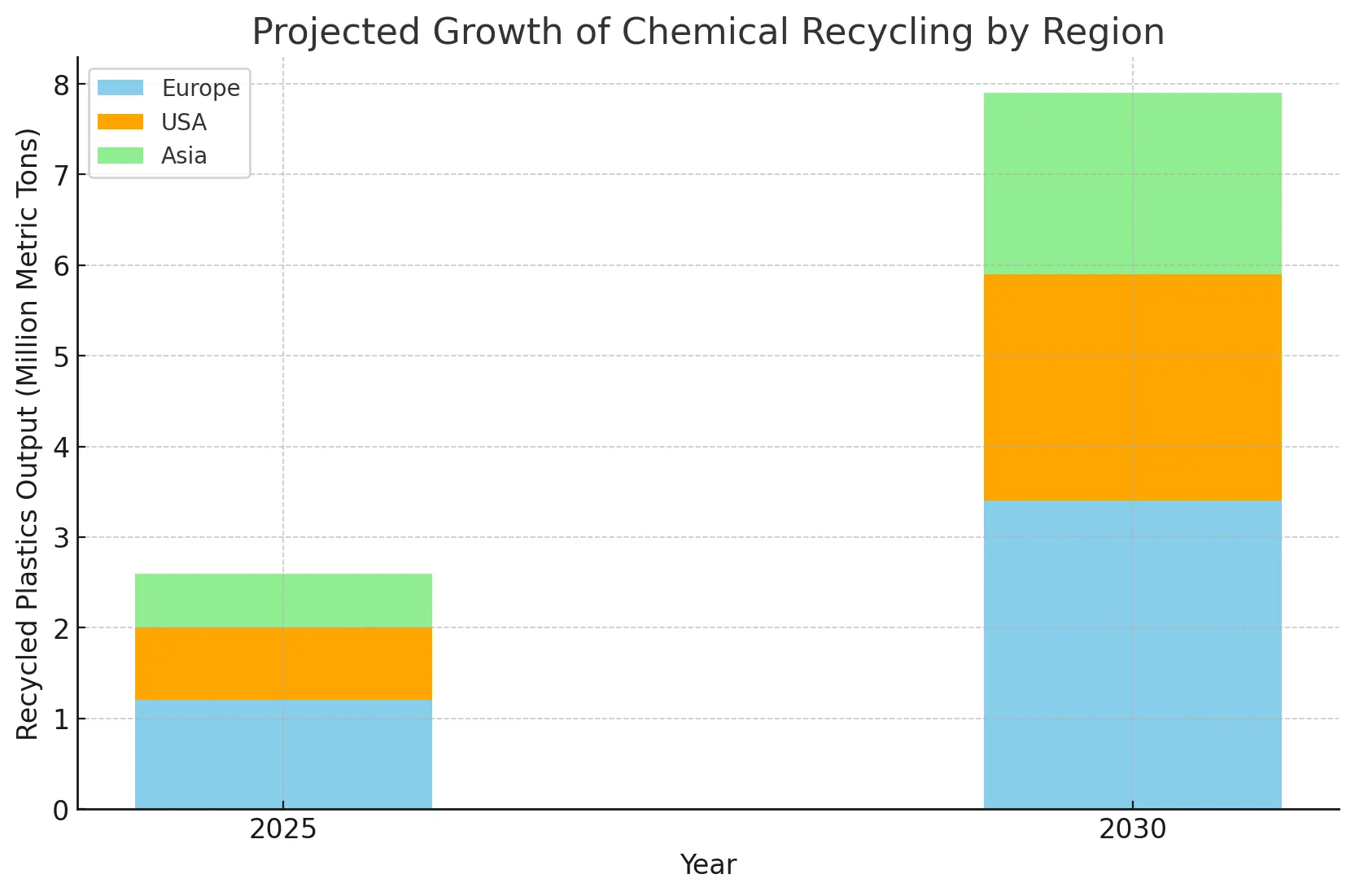

The chemical recycling market is projected to grow at 17-20% CAGR through 2035, with pyrolysis representing the dominant technology. This growth is driven almost entirely by EPR-linked policy: mandatory recycled content targets that only chemical recycling can fulfil at scale for food-contact and high-performance applications.

Major petrochemical companies — including BASF, Shell, SABIC, LyondellBasell, and TotalEnergies — are collectively investing over $10 billion in chemical recycling capacity, creating strong offtake demand for ISCC-certified pyrolysis oil.

Chemical recycling growth by region

EPR = Guaranteed Demand

Unlike voluntary sustainability initiatives, EPR mandates are legally binding. Non-compliance carries financial penalties, making EPR-driven demand far more reliable than market-based demand alone. For pyrolysis investors, this translates to reduced market risk and more bankable project economics.

APChemi pyrolysis plant — built for EPR-driven circular economy

Automated plant operations and monitoring

APChemi's EPR-Ready Solutions

APChemi designs and builds pyrolysis plants specifically engineered for the EPR-driven circular economy — producing petrochemical-grade output that meets regulatory requirements for recycled content claims.

ISCC Plus Certification

- ✓ 4 ISCC PLUS plants certified (+1 coming up) — proven track record

- ✓ Mass balance accounting for recycled content claims

- ✓ Chain of custody documentation and audit support

Petrochemical-Grade Output

- ✓ PYROMAX reactors engineered for maximum oil quality

- ✓ PUREMAX oil purification — naphtha-grade for steam crackers

- ✓ Virgin-quality output qualifying for recycled content

Regulatory Compliance

- ✓ Plant designs meeting EU, India, UK regulatory standards

- ✓ EPR compliance documentation support

- ✓ Environmental monitoring and reporting systems

Global Experience

- ✓ 49+ projects across multiple regulatory regimes

- ✓ 17+ years of pyrolysis industry experience

- ✓ 12+ patents in pyrolysis and oil purification

APChemi's ISCC-certified operations — EPR compliance-ready from day one

Environmental Impact — Beyond Compliance

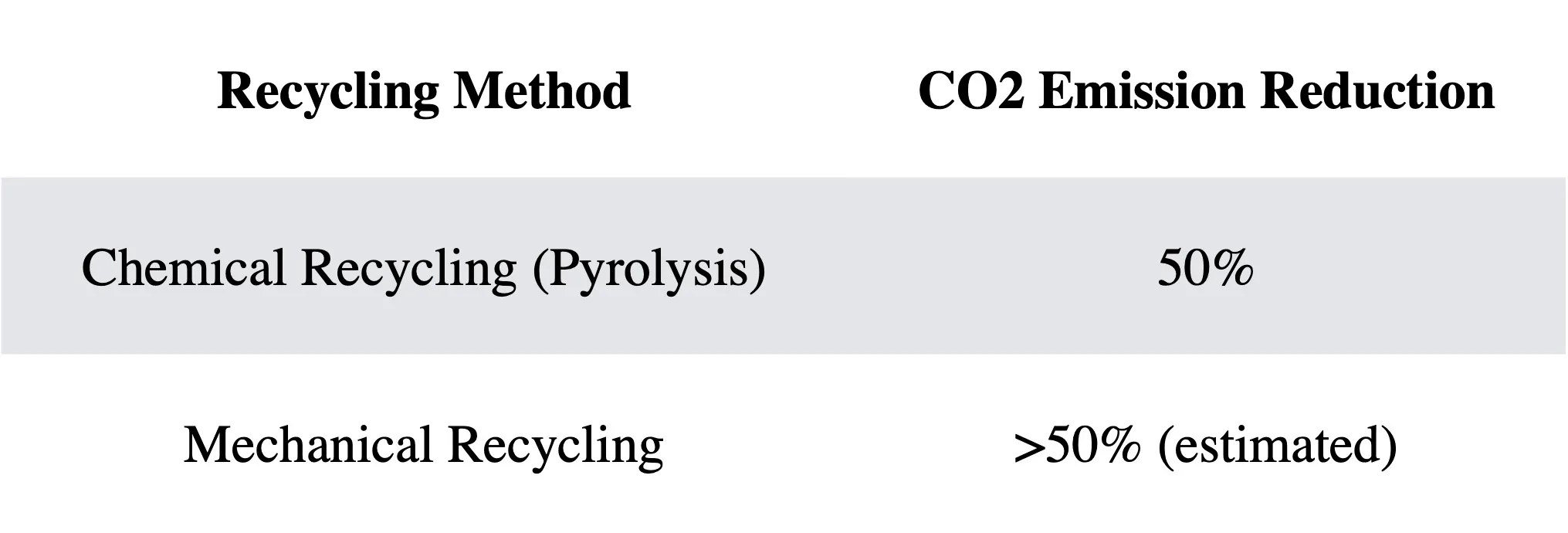

EPR-driven chemical recycling through pyrolysis delivers measurable environmental benefits beyond regulatory compliance. By diverting plastic from landfill and incineration to circular feedstock, pyrolysis reduces lifecycle CO₂ emissions by 50-70% compared to virgin plastic production. These verified environmental benefits strengthen project economics through carbon credits and ESG-linked financing.

Emissions reduction through pyrolysis

Frequently Asked Questions

EPR is a policy framework that shifts the financial and operational responsibility for end-of-life product management from municipalities to the producers (manufacturers, importers, brand owners) who place products on the market. Producers must fund collection, sorting, recycling, and disposal infrastructure — creating direct financial incentives to design for recyclability and invest in recycling technologies like pyrolysis.

EPR drives pyrolysis demand through three mechanisms: (1) increased feedstock supply — mandatory collection targets channel more waste plastic and tires into recycling systems, (2) recycled content mandates — regulations like the EU PPWR require minimum percentages of recycled content in new products, which only chemical recycling can meet for many applications, and (3) financial incentives — EPR fee modulation and plastic taxes create price signals favouring recycled materials.

Over 60 countries have implemented plastic EPR schemes. Key regions include: the EU (all 27 member states under the Packaging and Packaging Waste Regulation), India (Plastic Waste Management Rules with strict recycling targets), UK (packaging EPR with Plastic Packaging Tax), Canada (provincial EPR programs), and the US (7+ states including California, Colorado, Oregon, and Maine with enacted legislation).

Yes. Tire EPR is well-established globally. In the EU, 21+ countries have tire EPR schemes. India mandates 100% EPR for tires. The US state of Connecticut enacted tire EPR effective March 2026. Canada has provincial tire recycling programs. Pyrolysis is an approved processing method under most tire EPR schemes, producing pyrolysis oil, recovered carbon black (rCB), and steel.

Recycled content mandates require producers to include minimum percentages of recycled material in new products. The EU PPWR requires 10% recycled content in food-contact plastic packaging by 2030, rising to much higher targets by 2040. Mechanical recycling cannot produce food-grade recycled content for most plastics — making pyrolysis-based chemical recycling the primary pathway to compliance.

APChemi provides ISCC Plus certification support (required for mass balance accounting of recycled content), designs pyrolysis plants that produce petrochemical-grade oil suitable for circular feedstock markets, and helps clients position their operations to capture EPR-driven demand. Our experience with 4 ISCC PLUS-certified plants and 49+ projects globally ensures compliance-ready operations from day one.

Get a Free Consultation

Tell us about your pyrolysis project and our engineers will get back to you within 24 hours.

Get a Free Project Assessment →Explore More

Chemical Recycling

How pyrolysis enables plastic-to-plastic chemical recycling at scale.

ISCC Plus Certification

Certify your pyrolysis output for mass balance and recycled content claims.

Plastic Pyrolysis Plant

Convert waste plastics into pyrolysis oil for circular feedstock markets.

Tire Pyrolysis Plant

Tire-derived oil and rCB for circular rubber production under EPR.

Pyrolysis Plant Cost Guide

Investment analysis for EPR-driven pyrolysis plant projects.

Oil Purification & Distillation

Upgrade pyrolysis oil to naphtha-grade feedstock for petrochemical acceptance.